The Index strategy is based on qualitative and quantitative inputs including economic data and interpretations of government policy. Asset allocation guardrails include 50% – 200% allocation relative to the benchmark for credit, duration, and structure/mortgage weight. A high conviction exposure to more speculative or diversifying positions is constrained to 0% – 20%.

The characteristics below reflect how we would best position a portfolio of fixed-income ETFs to achieve maximum total return over a comparable baseline neutral portfolio of fixed-income securities (benchmark).

Relative Positioning

Duration

90% Duration

Yield Curve

Neutral

Corporate Credit

Underweight

Securitized

Underweight MBS

Conviction

20% 0-5 US TIPS

Rationale

90% Duration

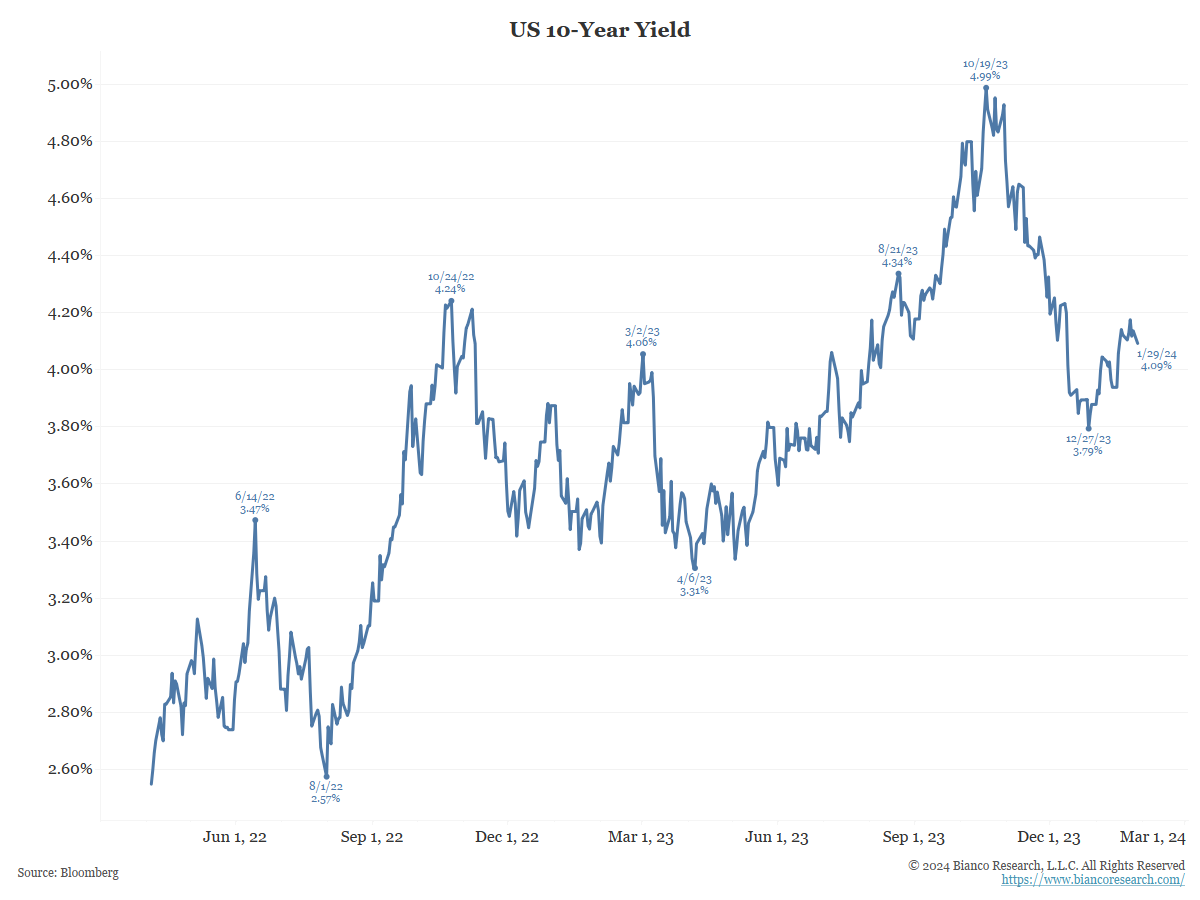

The index is underweight duration, based on the belief rates could head higher.

The 10-year yield was recently at a 16-year high. While yields have fallen since October, we do not believe this trend is over.

Neutral Curve Position

The Index holds no curve position relative to the benchmark.

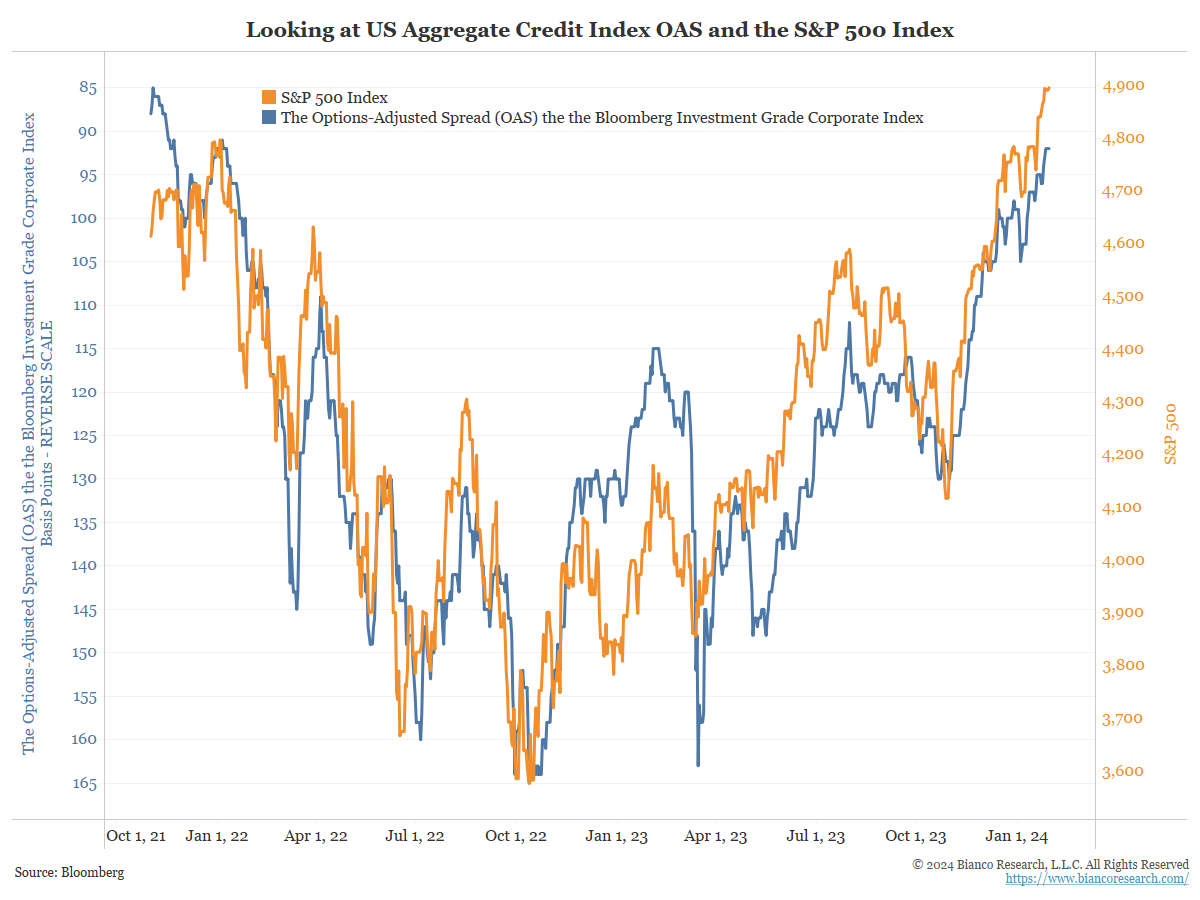

90% Underweight Credit

The index has a 90% allocation to corporates relative to the benchmark. In other words, the index holds an underweight allocation to corporate credit.

The chart shows investment-grade corporate spreads (blue) and the S&P 500 (orange) move in tandem. Relative credit performance moves with equity prices.

With stocks at all-time highs, and record corporate bond issuance in January, we are reducing our credit exposure from 100% to 90% as we see increased risks.

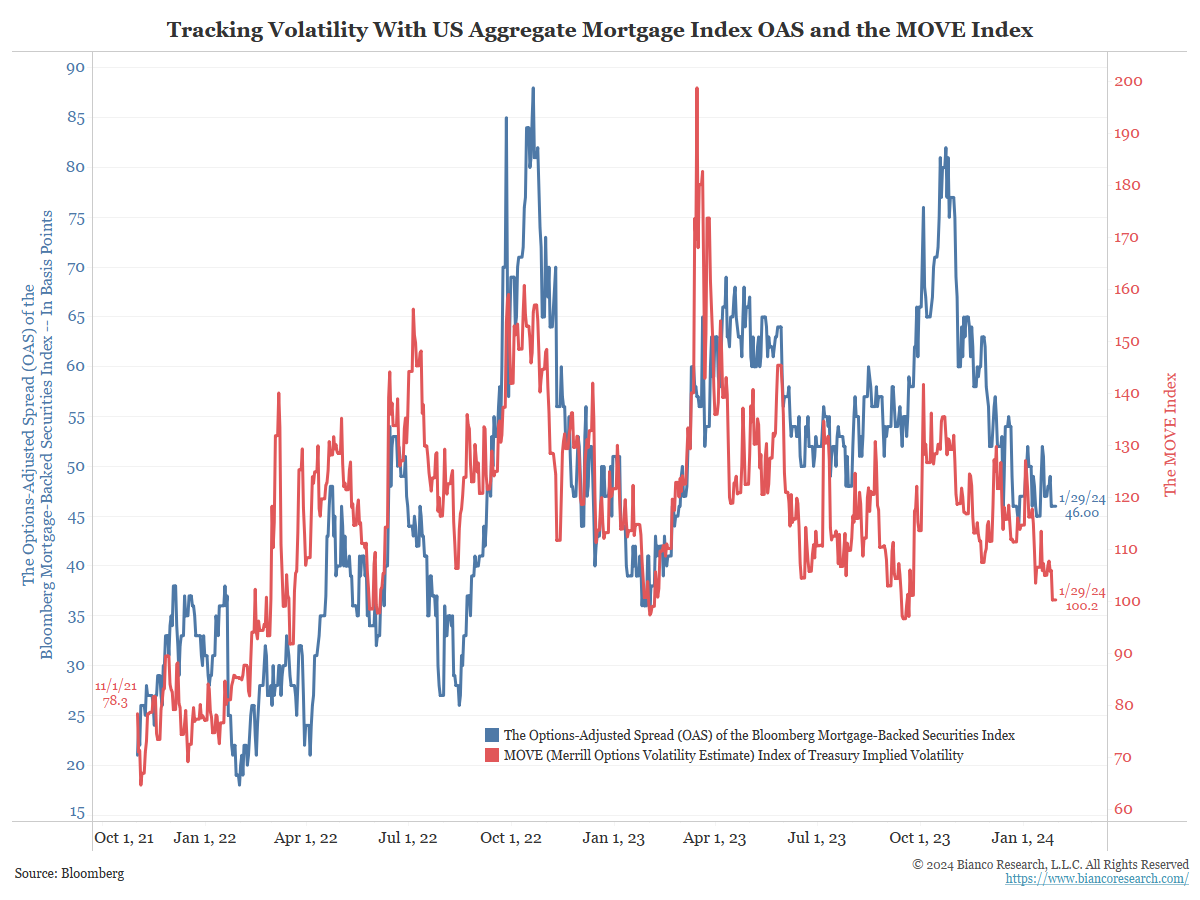

80% Underweight Securitized

All mortgages have an embedded option because holders can pre-pay their mortgage anytime. Because of this structure, the option-adjusted spread (OAS) of mortgages (blue line) and the MOVE Index (red line), which measures the implied volatility of 30-day interest rate options, have a tight relationship.

Given the uncertainty surrounding inflation, Fed policy, and the belief that rates will move higher, look for the yield curve to bear steepen. This can “un-invert” the yield curve in the coming months, and provide a tailwind to mortgage relative performance.

We remain underweight at 80% relative, up from 72% last month.

20% TIPS Conviction Allocation

The index holds a 20% allocation to 0-5 year TIPS as inflation protection.

The index owns short-maturity inflation securities (TIPS). The 2-year inflation break-even rate has held between 200 and 230bps. The committee anticipates inflation to exceed this level over the next two years. Short-maturity inflation protection is attractive, especially if inflation remains sticky and persistent.

Allocation Changes

| Name | February 2024 | January 2024 |

|---|---|---|

| iShares MBS ETF | 23.30 | 21.00 |

| iShares 0-5 Year TIPS Bond ETF | 20.00 | 20.00 |

| Vanguard Long-Term Corporate Bond ETF | 8.14 | 9.00 |

| WisdomTree Floating Rate Treasury ETF | 8.00 | 8.00 |

| Vanguard Short-Term Corporate Bond ETF | 7.24 | 8.00 |

| Schwab Long-Term U.S. Treasury ETF | 7.00 | 7.00 |

| Vanguard Intermediate-Term Corporate Bond ETF | 6.41 | 7.09 |

| Schwab Short-Term U.S. Treasury ETF | 5.91 | 5.91 |

| iShares 7-10 Year Treasury Bond ETF | 5.50 | 5.50 |

| iShares BBB Rated Corporate Bond ETF | 5.00 | 5.00 |

| iShares 3-7 Year Treasury Bond ETF | 3.50 | 3.50 |