The Index strategy is based on qualitative and quantitative inputs, including economic data and interpretations of government policy. Asset allocation guardrails include 50% – 200% allocation relative to the benchmark for credit, duration, and structure/mortgage weight. A high-conviction exposure to more speculative or diversifying positions is constrained to 0% – 20%.

The characteristics below reflect how we would best position a portfolio of fixed-income ETFs to achieve maximum total return over a comparable baseline neutral portfolio of fixed-income securities (benchmark).

Relative Positioning

Duration

90% Relative Underweight

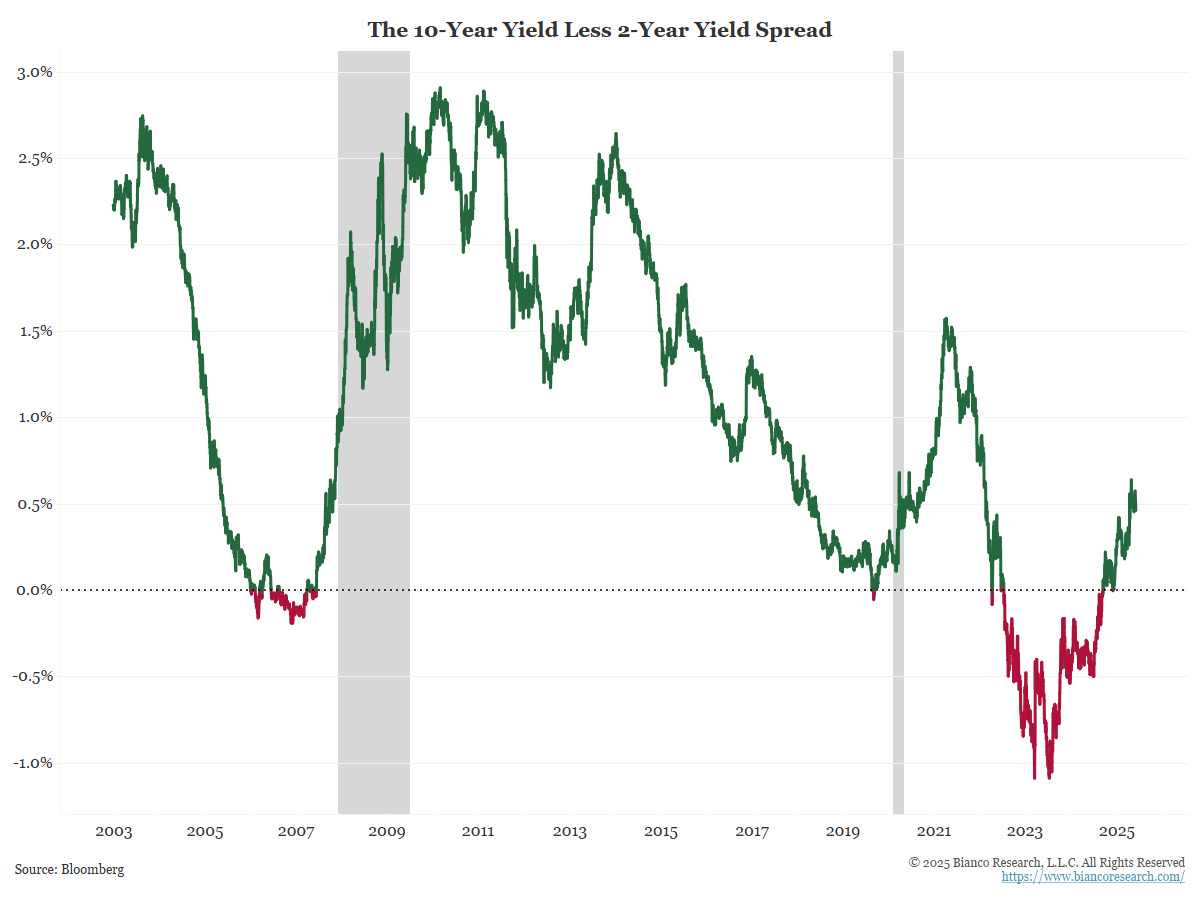

Yield Curve

Slightly Bulleted

Corporate Credit

Underweight

Securitized

Overweight

Conviction

10% EM Local Debt & 5% Short TIPS

Rationale

90% Duration

The Index holds 90% relative duration position compared to its benchmark, positioning for a rise in interest rates.

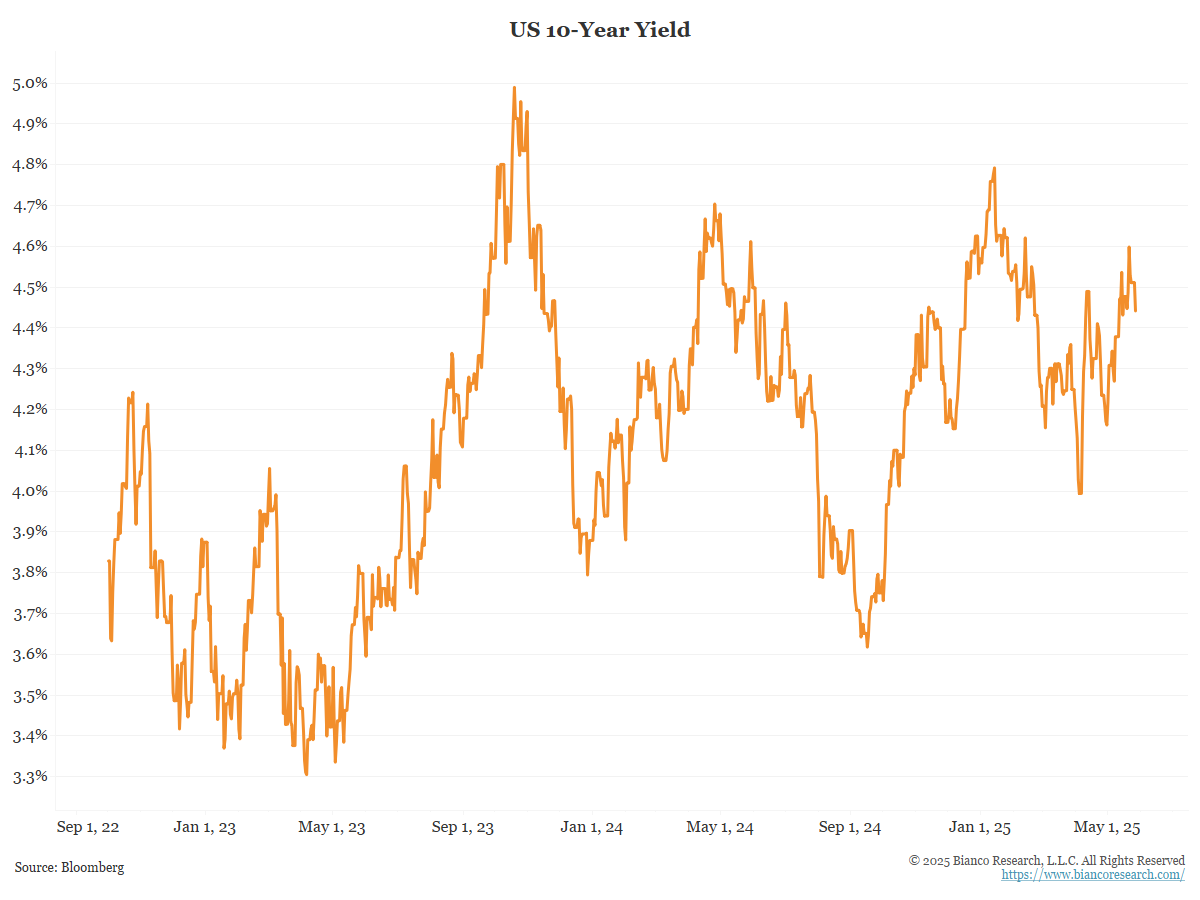

The committee expects the economy and inflation to remain stronger than expected. Recent talk of recession, tariffs, and 10% stock market corrections should have produced lower rates. Yet, the 10-year yield remains well above its low of 3.60% last September. We continue to believe that this bond-bullish news will soon give way to bond-bearish news, indicating a stronger economy and sticky inflation.

Slightly Bulleted Curve Position

The Index holds a bulleted curve position relative to the benchmark. This means it is overweight in the middle of the yield curve. This position will benefit from the yield curve steepening.

If inflation remains sticky, we expect long-term yields to rise faster than short-term yields, thereby steepening the yield curve.

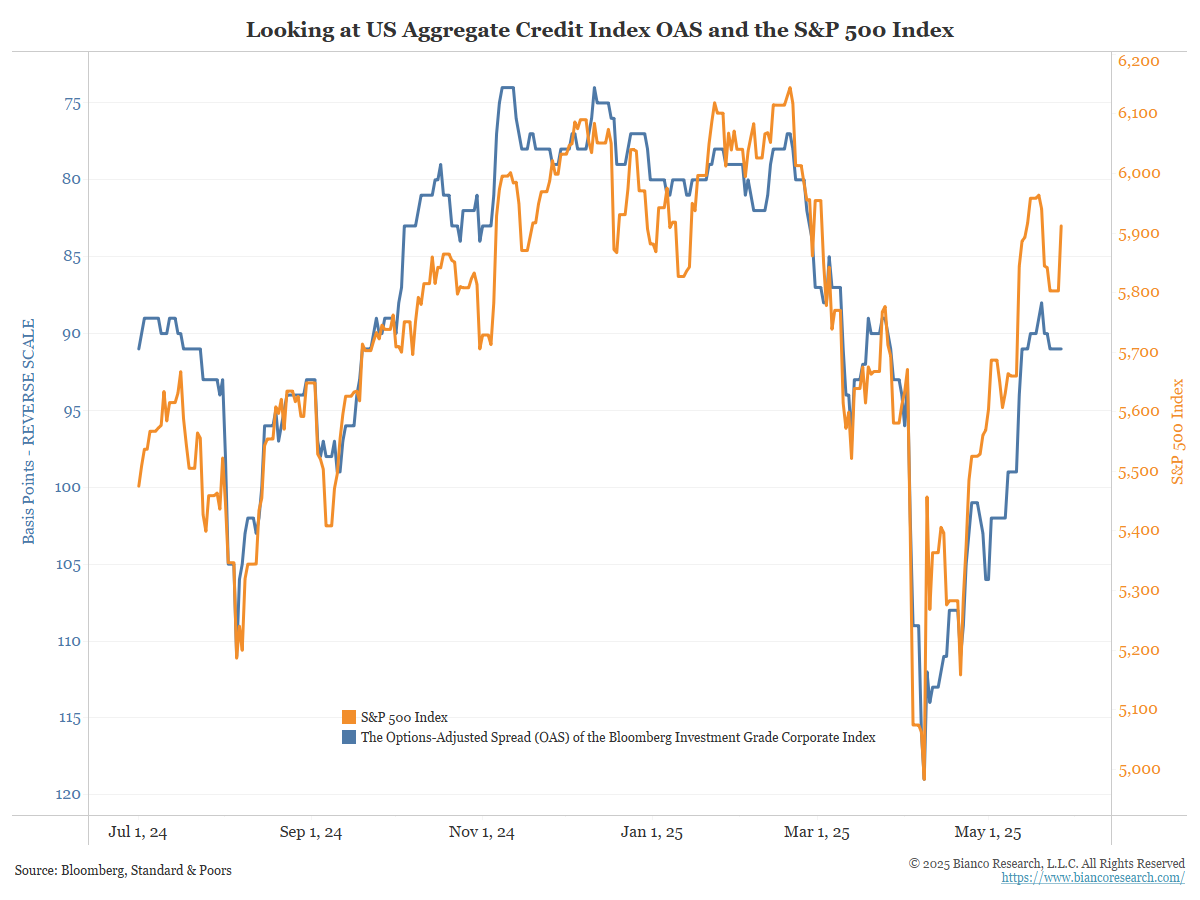

70% Underweight Credit

The Index is 70% weighted in corporate bonds relative to the benchmark, given strong corporate bond issuance (an increase in supply) and high valuations in the equity market.

Relative corporate bond positions are correlated to stock market movements.

120% Overweight MBS

The committee decided to decrease the overweight in mortgage-backed securities (MBS) from 140% to 120% of the benchmark allocation in June.

MBS yields are significantly higher than Treasury yields and comparable to those of investment-grade corporate bonds.

Rising Treasury yields will benefit MBS by slowing the rate of refinancing, keeping MBS yields high, and limiting any price declines.

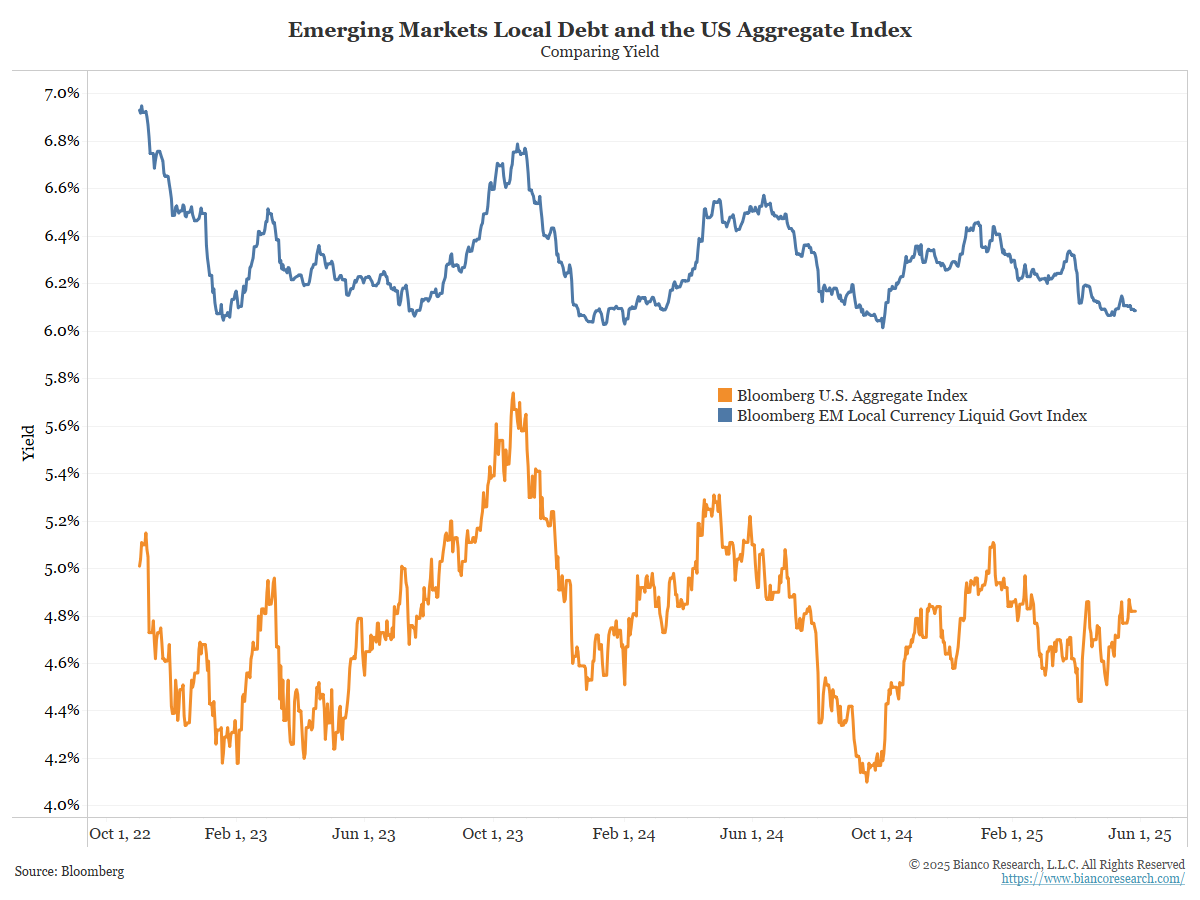

10% EM Local Debt & 5% Short TIPS

In April 2025, the committee allocated 10% to emerging market local debt and continues to hold this position.

This position offers a higher yield than domestic corporate bonds and will benefit from a weakening dollar relative to these currencies. This has been the case so far this year, and we anticipate it will continue in the same manner.

In June, the committee elected to add a 5% position in short (0-5) TIPS securities. This position will offer inflation protection at an attractive yield.

Allocation Changes

| Name | June 2025 | May 2025 |

|---|---|---|

| iShares MBS ETF | 32.00 | 40.50 |

| iShares 3-7 Year Treasury Bond ETF | 14.40 | 11.90 |

| iShares 7-10 Year Treasury Bond ETF | 12.50 | 10.00 |

| WisdomTree Emerging Markets Local Debt Fund | 10.00 | 10.00 |

| Vanguard Short-Term Corporate Bond ETF | 9.70 | 9.00 |

| Schwab Short-Term U.S. Treasury ETF | 5.00 | 6.50 |

| iShares 0-5 Year TIPS Bond ETF | 5.00 | 0.00 |

| iShares BBB Rated Corporate Bond ETF | 4.50 | 4.50 |

| Vanguard Intermediate-Term Corporate Bond ETF | 4.00 | 5.60 |

| Schwab Long-Term U.S. Treasury ETF | 1.50 | 1.00 |

| Vanguard Long-Term Corporate Bond ETF | 1.40 | 1.00 |